UK rail productivity is continuing its steady recovery from the pandemic, but the latest data from ORR underlines a more complex reality: while output is rising, the cost of running the railway remains stubbornly high, and the gap to historic efficiency levels has not yet been fully closed.

The Office of Rail and Road’s (ORR) 2026 Rail Industry Productivity Report points to a third consecutive year of improvement, with overall productivity increasing by around 3% in 2024–25. The uplift reflects a system carrying more passengers and running more services without a corresponding rise in expenditure.

Passenger journeys rose by 7% year-on-year, while train kilometres increased by 5%. This return of activity has been the primary driver behind the improved productivity figures, signalling a network gradually regaining its footing after the sharp contraction seen during 2020 and 2021.

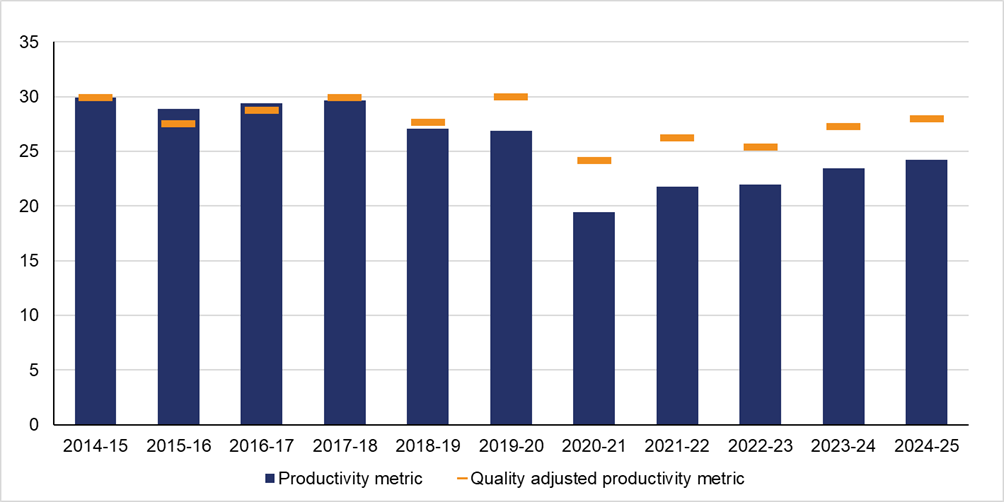

Yet the recovery remains incomplete. Despite recent gains, the railway is still producing around 6% less output per pound spent than it did a decade ago. The direction of travel is positive, but the industry has not yet returned to its pre-pandemic efficiency baseline.

Recovery driven by activity, not structural change

At its core, the productivity rebound has been driven by demand returning rather than a wholesale transformation in how the railway operates. With costs broadly stable in real terms over the past year, increased service levels have translated directly into modest efficiency gains.

However, the longer-term picture is less forgiving. Total rail expenditure is now around 21% higher in real terms than it was ten years ago. Even as emergency pandemic funding recedes, government support remains well above historical norms, reinforcing the scale of the financial challenge still facing the sector.

This imbalance between rising costs and only gradual efficiency improvements has sharpened the focus on value for money. The industry is no longer operating in an environment where additional funding can offset inefficiencies; instead, it must demonstrate tangible gains in output for every pound spent.

Two measures, two narratives

A key feature of the ORR report is its distinction between headline productivity measures and Total Factor Productivity (TFP), which together offer different interpretations of industry performance.

Headline metrics, such as train kilometres per unit of expenditure, present a straightforward view: the railway is still less efficient than it was a decade ago. These measures reflect the reality felt most directly by operators and infrastructure managers, where rising costs continue to weigh on budgets.

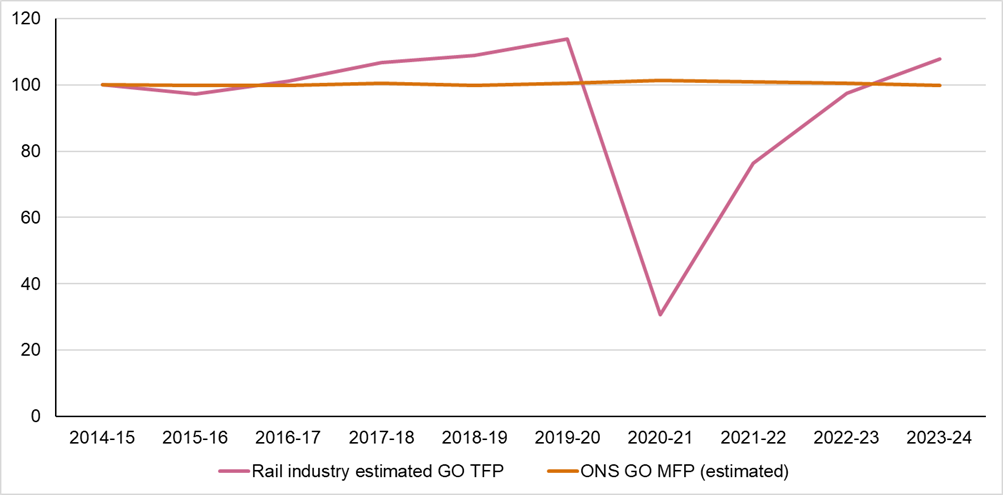

TFP, by contrast, paints a more optimistic picture. By accounting for all inputs simultaneously, including labour, operating costs and capital assets, it captures broader system efficiency. On this basis, productivity rose sharply by 11% in 2023–24 and now sits around 8% above 2014–15 levels.

The divergence between the two measures is significant. TFP reflects improvements in how resources are combined, including the impact of asset utilisation and changes in capital value. Headline measures, meanwhile, remain anchored in the day-to-day economics of running services.

Both matter. For policymakers and long-term planning, TFP suggests the industry is capable of delivering efficiency gains when viewed holistically. For operators and suppliers, headline productivity remains the more immediate concern, shaping funding decisions and operational constraints.

Cost control moves centre stage

With expenditure elevated and public funding under scrutiny, the report reinforces a clear message: cost discipline is no longer optional.

The government has signalled a decisive shift away from pandemic-era support, with a stronger emphasis on affordability and efficiency. While subsidy levels are gradually declining, they remain high enough to sustain pressure from both the Treasury and the Department for Transport.

For rail businesses, this translates into a more demanding operating environment. Investment is increasingly focused on maintaining and optimising existing assets rather than pursuing large-scale expansion. Programmes aimed at improving internal efficiency, reducing waste and tightening delivery are becoming central to organisational strategy.

Network Rail’s ongoing efficiency drive is one example of this shift, targeting cost reductions without compromising core operations. For suppliers, the implications are equally clear: contracts will increasingly favour those who can demonstrate reliability, cost certainty and measurable value.

The industry is moving into a phase where performance will be judged less on ambition and more on execution. Delivering projects on time, within budget and with clear outcomes is becoming the defining requirement.

Reform on the horizon

Overlaying these operational pressures is the structural reform set to reshape the industry. The creation of Great British Railways (GBR) represents the most significant reorganisation of the railway since privatisation, aiming to bring infrastructure and operations under a single guiding authority.

Legislation progressing through Parliament will give GBR control over infrastructure, service planning, contracting and ticketing. In parallel, the gradual transition of services into public ownership is already underway, with the majority expected to be operated under government control by 2026.

The intended outcome is a more integrated system, capable of making coordinated decisions across track and train. In theory, this should reduce duplication, streamline processes and improve overall efficiency.

However, the transition will take time. In the near term, existing structures remain in place, and businesses should not expect immediate changes to procurement or delivery models. The full operational impact of GBR is unlikely to be realised until later in the decade.

Preparing for a different model

For rail companies, the challenge is to navigate two parallel realities. In the short term, the focus must remain on improving efficiency within the current system. In the longer term, organisations need to position themselves for a more centralised and strategically driven industry.

This will require adaptability. As GBR’s priorities become clearer, businesses will need to align with new expectations around collaboration, performance and long-term value. The shift towards a single guiding authority is likely to bring greater consistency, but also greater scrutiny.

Engagement with emerging regional structures and early initiatives will be critical. Those that understand and respond to the direction of travel are likely to be better placed when new frameworks are fully established.

A sector at a turning point

The latest productivity data captures a railway in transition. Recovery is underway, supported by returning demand and stabilising costs. Yet the legacy of higher expenditure and the need for sustained efficiency gains remain pressing concerns.

At the same time, structural reform is reshaping the landscape in which the industry operates. The move towards integration offers the potential for long-term improvements, but it does not remove the immediate need for tighter cost control and better performance.

For rail businesses, the message is clear. Productivity is no longer a background metric; it is central to competitiveness and sustainability. Those that can deliver more with less, while adapting to a changing system, will define the next phase of the industry.

The opportunity is there. The question is whether the sector can turn incremental gains into lasting change.

{kind=link}