The latest statistics from the Office of Rail and Road (ORR) have painted a mixed picture of the UK rail industry’s financial performance.

Key Findings:

- Passenger Journey Recovery: Passenger journeys increased by 16% to 1.6 billion, demonstrating a continued recovery from the pandemic. However, this figure remains 7% below pre-pandemic levels.

- Fare Revenue Growth: Fare revenue rose by 14% to £10.4 billion, driven by increased passenger numbers. Yet, it still lags 18% behind pre-pandemic levels.

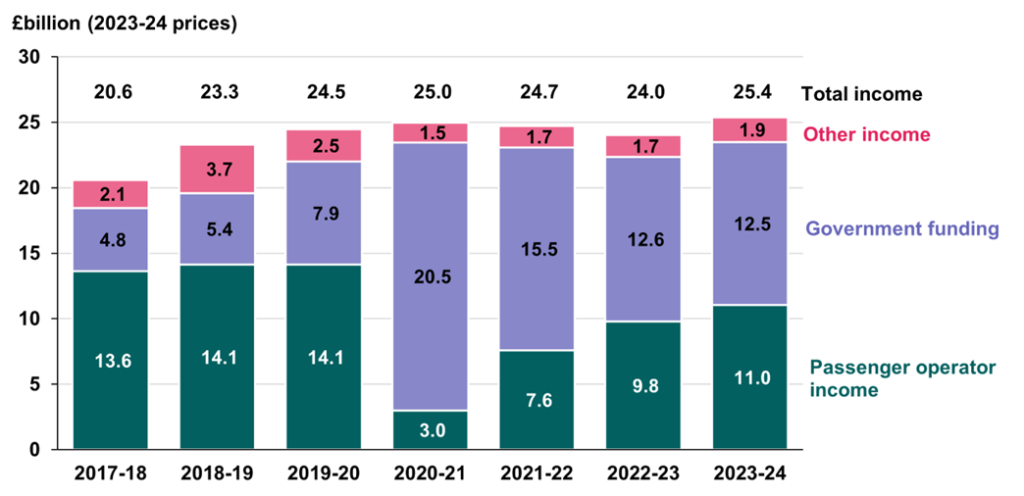

- Government Funding: Government funding for the railway’s day-to-day operations decreased by 1% to £12.5 billion, now accounting for 49% of operational income.

- Industry Expenditure: Operational industry expenditure decreased by 7% to £25.1 billion, with a slight increase in infrastructure and rolling stock investment, primarily driven by HS2.

- ROSCO Profit Margins: Rolling stock companies (ROSCOs) experienced a 12% decline in net profit margins, and dividend payouts decreased by 39%.

Will Godfrey, Director of Economics, Finance and Markets said: “Our official statistics are an important barometer of the financial health of Britain’s railways. In the latest year, passenger journeys and fares revenues continued to increase, but remain short of pre-pandemic levels.

“Our figures also show that government support remains substantial, at just under half of income for the day to day running of the railway.”

These findings highlight the ongoing challenges faced by the UK rail industry, as it strives to fully recover from the pandemic’s impact and adapt to evolving passenger needs and economic conditions.

{kind=link}